Buying a home is like planning the road trip of a lifetime … except when someone hands you the keys and points you toward the horizon, they also slip a blindfold over your eyes. Sure, you can already picture the destination clearly: the tree-lined street of your dreams, the morning light hitting your kitchen just right, the neighborhood that feels like it was made to fit you. But knowing where you want to end up isn’t the same as knowing how to get there.

That’s why it’s vital that you have the right people and tools to guide you. A Mortgage Loan Officer (aka a lender), real estate agent, underwriter, and title/escrow company will help you take off the blindfold and understand each stretch of the trip before you ever shift into drive.

Ready for an easy-to-read map of the homebuying journey? Look no further.

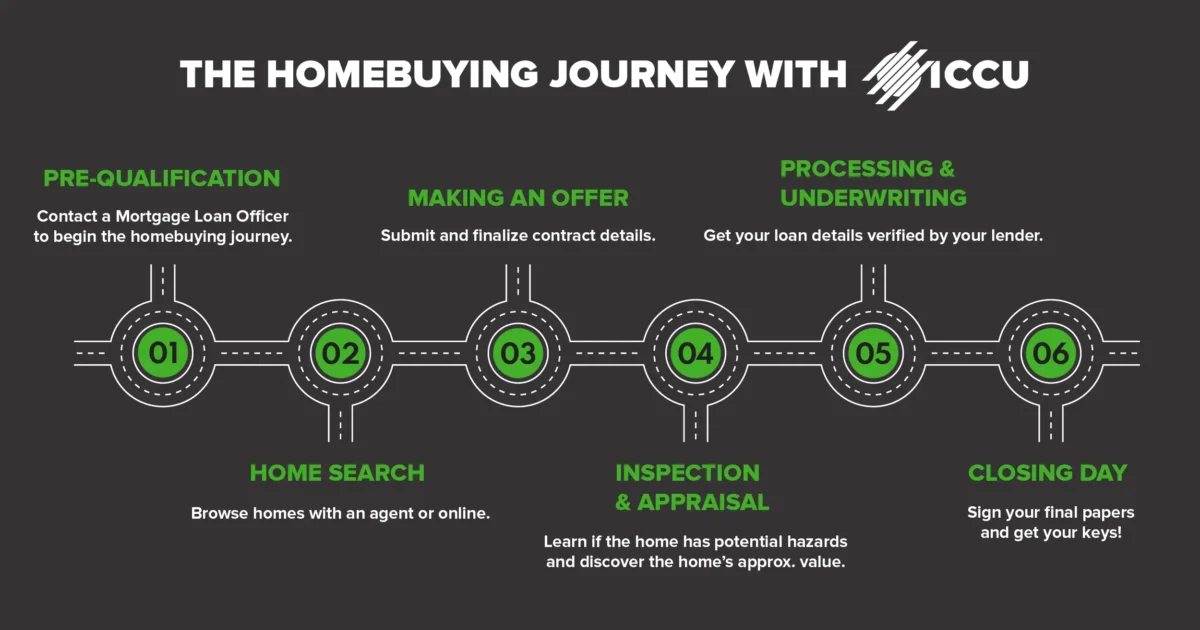

The Homebuying Journey at a Glance

- Start by contacting a Mortgage Loan Officer, who will initiate your pre-qualification. They’ll ask you to provide a handful of financial documents so they can get a big picture of your financial situation.

- Search for your new home by working with a real estate agent. House hunting apps can also be a good resource.

- Make an offer on your favorite home, working with your agent to get the details right. Here you can nail down the specifics of your contract.

- Get a home inspection and appraisal. The inspector will review the property for any potential hazards, and if they find issues, you may have a chance to renegotiate, depending on the contract’s terms.

- Get your loan processed and underwritten through your Mortgage Loan Officer. An underwriter will be assigned to you, and they will ensure all the details in your loan are accurate.

- Attend your closing appointment with your homebuying team. Soon after you sign the final documents, you’ll get the keys to your new home!

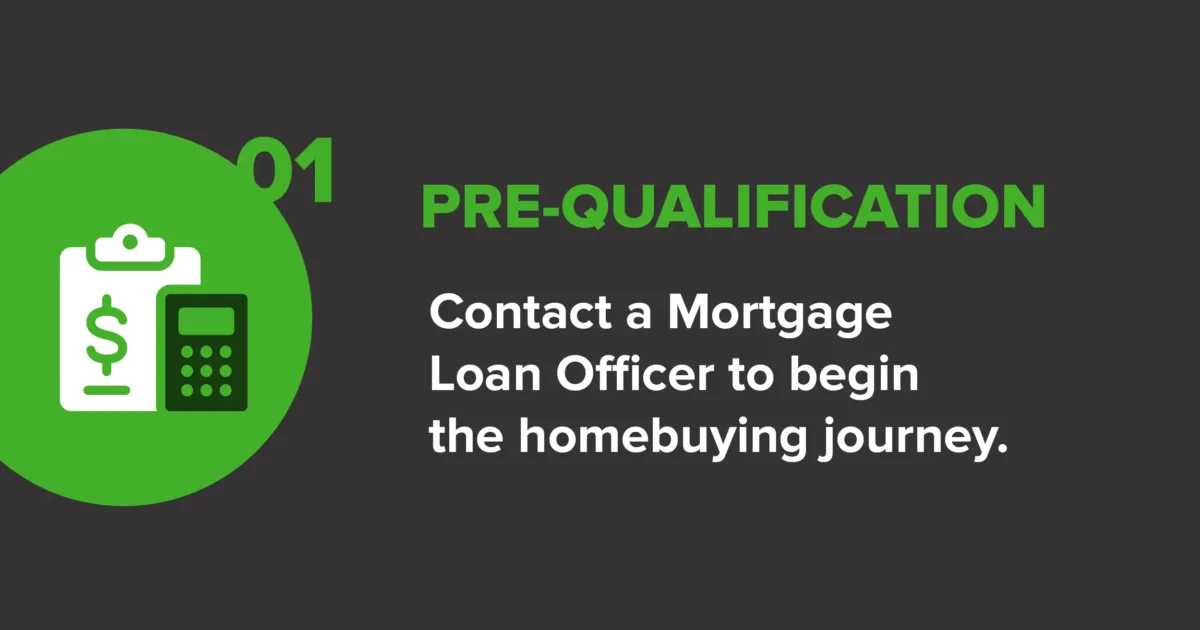

Pre-Qualification

Your guide: A Mortgage Loan Officer

Before you scroll through endless home listings (tempting, we know), it helps to get a picture of what you can afford. Enter the pre-qualification phase.

How Do You Pre-Qualify for a Mortgage?

Reach out to a Mortgage Loan Officer to get started. They’ll ask for a variety of financial documents so they can get a snapshot of where you stand now and what your buying power likely is. There’s a good chance you’ll be asked to provide:

- Income info from recent pay stubs, W-2s, or estimates of additional income like bonuses and commissions.

- Employment details like who you’ve worked for and how long (if you’re self-employed, we’ll typically ask for two years of business income.)

- Asset info like checking, savings, and retirement account balances.

- Debts on credit cards, auto loans, student loans, liens, etc.

If you’re not sure where to find these documents and you bank with ICCU, we can help. Call 1-800-456-5067, jump on a VideoChat, or visit your nearest branch for more guidance. If you’ve already applied and have chosen or been assigned an ICCU Mortgage Loan Officer, you can reach out directly to them.

Ultimately, the Mortgage Loan Officer looks at what funds you have, how stable your finances are, and how much you currently owe to others. That helps them establish a baseline lending risk (aka how likely you are to pay back your loan) and find a buying range that will fit you best.

Tip: Once you start the homebuying process, it’s generally wise to hold off on big financial decisions like buying a new car or opening a credit card because that might alter or invalidate your pre-qualification.

Home Search

Your guide: An experienced real estate agent

This is where the homebuying journey gets fun. You know your buying power and have envisioned your dream home — now let’s find it.

Many people start with house hunting apps. Pick a handful of favorite properties and contact your real estate agent to schedule an in-person visit. Alternatively, you can skip the apps and tell your agent directly about your must-haves and dealbreakers. They’ll find you a slew of options.

How Do You Find a Good Real Estate Agent?

Finding the right real estate agent is less about flashy ads and more about fit, experience, and trust. Many people meet their agent through word-of-mouth. If any of your friends and family members have bought a house recently, ask them about their experience.

A few questions to get you started:

- What did your agent do well?

- How was their communication?

- Would you work with them again? Why or why not?

Remember, your Mortgage Loan Officer is a great resource. They often work with agents in the area and can recommend a few experienced agents.

Making an Offer

Your guide: Your real estate agent

Now let’s turn that dream home into reality. Work with your real estate agent to make an offer on the home. This usually includes:

- The purchase price: what you’re willing to pay for the home. It can be at, above, or below the asking price.

- Financing terms: the specifics on how you’ll pay for the home. You’ll see things like loan type (conventional, FHA, VA, USDA, first-time homebuyer loans, etc.), the down payment amount, and whether the offer is contingent on loan approval.

- Contingencies: conditions that must be met before the sale is finalized. In less competitive markets, for example, you may be able to add a Sale of Buyer’s Home Contingency, which means that you’re only committed to buying the new home when your existing one has sold.

- Inspection terms: when a home inspector will visit to check the quality of the house. This typically happens within 7-14 days. If the home inspector finds issues in the house (for example, mold), then as a buyer, you can request repairs, ask for credits, or walk away from the sale.

- Closing and possession dates: when the sale will finalize and when you get the keys. Often, the closing and possession dates are the same.

- Items included or excluded: the things you can expect to stay with the home when you buy it. Some sellers prefer to leave certain belongings behind, like fridges and sheds, while others expect to take it with them when

thethey sell the house. Deciding what stays and goes now will prevent misunderstandings later. - Seller concessions (if applicable): any fees or repair credits you’re asking the seller to pay. This is often where you negotiate who pays closing costs.

If that sounds like a lot, that’s because it is. But don’t worry, a good real estate agent will explain each of these things in detail to you. You can ask your agent as many questions as you like (in fact, we encourage it) before sending your offer. Each offer will be different and may require a different strategy. That’s why it’s so important to select an agent with experience.

Home Inspection and Appraisal

Your guide: Your real estate agent

If the seller accepts your offer, your real estate agent will help you schedule an appointment with a licensed home inspector, and if you’re financing the purchase, a professional appraisal. Inspections are usually completed within a set contingency period outlined in your purchase agreement (often 7–14 days). The inspector will conduct a visual, non-invasive review of the home to ensure that issues are disclosed to you.

Around the same time, your lender will order a home appraisal to confirm the home’s market value. The appraiser evaluates the property and compares it to similar recent sales in the area.

If the inspection uncovers major problems or the appraisal comes in lower than the purchase price, you may be able to renegotiate with the seller, request repairs, or walk away from the contract, provided you have inspection and appraisal contingencies.

How Long Does a Home Inspection Take?

Depending on the size and age of the property, an inspection often takes 2-4 hours. As a buyer, you’re encouraged to attend the inspection so you can ask questions and see issues firsthand, though it’s not required. The inspector will give you an in-depth document of their findings.

How Much Does a Home Inspection Cost?

Most home inspections cost between $300 and $600, but that number can change depending on a variety of factors, including the agreed-upon terms in your new contract. If you need or choose specialized inspection packages like radon testing, pest inspections, and more, that price could increase.

The buyer typically pays for the inspection, but again, that depends on the terms in your contract.

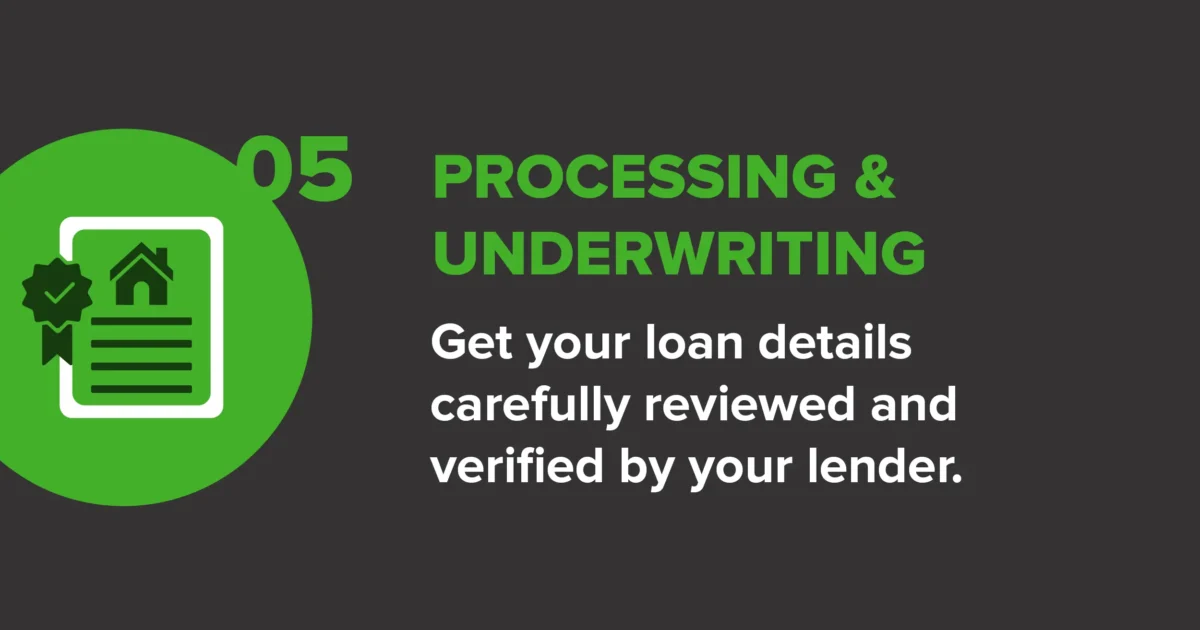

Processing and Underwriting

Your guide: Your Mortgage Loan Officer (and their underwriting team)

Once your offer is in and accepted, your loan shifts to processing and underwriting, the stage where everything you’ve already shared gets a closer, more careful look. Your Mortgage Loan Officer will assign a trained underwriter to your loan. This mostly happens behind the scenes, so expect to hear updates from your loan officer, not the underwriter.

What is a Mortgage Underwriter?

An underwriter carefully reviews the info in your loan file to make sure everything is accurate and the lending risk is low. Think of the pre-qualification as an estimate (like a tentative thumbs up) and the underwriting approval as the official green light.

(Because underwriting is a time-consuming, complex process, lenders start with a pre-qual and move to underwriting after you’re fully committed to buying the house — usually after the home inspection. That way, neither your time nor the underwriter’s is wasted.)

Will the Underwriter Ask for More Documents?

It’s very common for underwriters to request a follow‑up or two. That doesn’t mean anything is wrong. Often, they just need:

- A page that didn’t upload

- An updated version of a document

- A bit more clarity around a deposit or account

How Long Does Processing and Underwriting Take?

Together, processing and underwriting can take anywhere from a few days to a 2-3 weeks. The timing can shift depending on things like your loan type, how quickly documents are returned, and when the appraisal comes in. Your Mortgage Loan Officer will keep you updated so you’re not left wondering what’s happening behind the scenes. If something is needed from you, be sure to respond quickly to help keep everything moving at a steady pace.

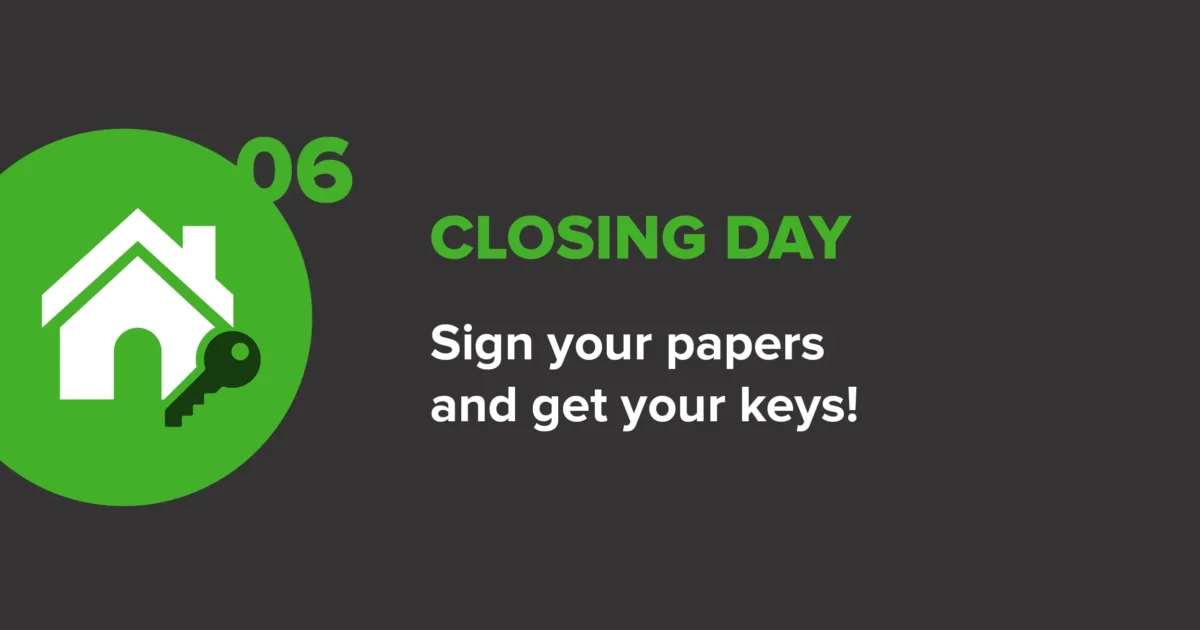

Closing Day

Your guide: Your Mortgage Loan Officer, real estate agent, and title/escrow company

Closing day is the final step of the homebuying journey, and while it’s a huge milestone, it’s also less complicated than it sounds. By this point, most of the hard work has been done. During closing, you simply review and sign final documents, then officially complete the home purchase.

This is also where your homebuying team will gather in person. Expect to see your Mortgage Loan Officer, real estate agent, and title/escrow company. Don’t worry about coordination; your team will do that for you. Alternatively, some lenders (like ICCU!) offer electronic closing options so you can securely sign your documents without leaving your home.

What Should You Bring to Closing?

Your Mortgage Loan Officer or closing agent will let you know exactly what’s needed, but you may be asked to bring a valid, government-issued photo ID and any required funds for closing.

Can You Move In on Closing Day?

In many cases, yes, you can. That said, your agent will confirm it with you beforehand. The sale is technically official after:

- All required documents are signed

- Your lender funds the loan

- The title or escrow company records the transaction

This usually happens on the same day or one business day after the closing appointment.

How Long Does Closing Take?

The closing appointment itself (where you review and sign the documents) usually takes 30-60 minutes. We recommend giving yourself a 90-minute window so you don’t feel rushed.

You’re More Prepared than You Think

Buying a home doesn’t have to feel like driving blind. As soon as you understand the route — pre-qualification, home search, making an offer, underwriting, closing —the homebuying journey becomes manageable and, dare we say, exciting.

Remember, you’re not expected to memorize every rule or anticipate every turn. A Mortgage Loan Officer helps set expectations and make sure you know what’s coming next. That way, buying a home will feel the way it’s supposed to: like the trip of a lifetime.

Blindfold off. Map in hand. Let’s get you home.

Equal Housing Lender.