For one in three college students, earning a higher education means walking off that stage with a diploma … and student loan debt. If a student loan is in your future, that might feel like a daunting statistic, but it doesn’t have to be. Like most forms of debt, a student loan may be a good choice — helping you get ahead in your career and access higher wages — so long as you do your research and find a loan and repayment strategy that fits you.

So let’s start with the basics. Most student loans fall into one of three categories: subsidized, unsubsidized, and private. By knowing each type’s structure, pros and cons, and eligibility requirements, you’re setting yourself up for future success.

Subsidized Loans

Offered by: the federal government

Pros: These loans don’t build interest until six months after you graduate.

Cons: Eligibility requirements are stricter, often based on financial need.

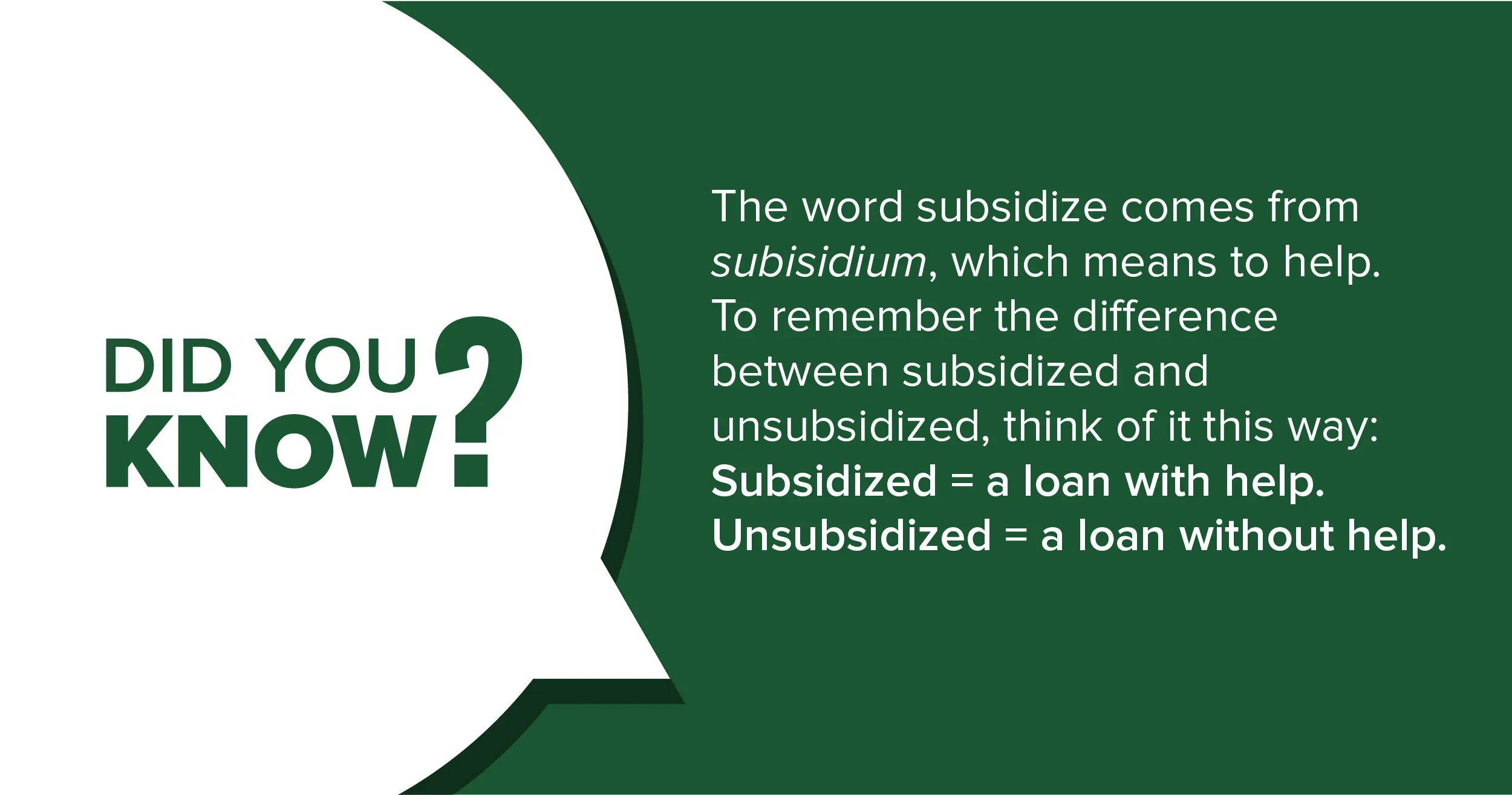

For most loans, including auto and home, your interest accrues as soon as you get it. Subsidized loans are different. Because they’re generally given to people who have a strong financial need, the government pays your interest until six months after you graduate — otherwise known as a grace period. After that, you’re expected to start making monthly payments.

Subsidized loans are available for 150% of the length of your program/degree. For example, if you enrolled in a four-year program, you’d be eligible to receive subsidized loans for six years. If you enrolled in a two-year program, you’d be eligible to receive subsidized loans for four years.

If you see that you’re eligible for subsidized loans, you should generally choose these before taking out other types of loans, which offer fewer benefits. See if you’re eligible by visiting studentaid.gov.

Unsubsidized Loans

Offered by: the federal government

Pros: These loans are available to many borrowers. If you don’t qualify for subsidized loans because of your (or your parents’) finances, you’ll likely qualify for unsubsidized loans.

Cons: Interest accrues while you’re in school. They typically have higher interest rates than subsidized ones.

When you take out an unsubsidized loan, you’re taking out a loan with fewer perks than a subsidized one. Starting the first day of disbursement, aka the day you receive your funds, your loan accrues interest.

Like a subsidized loan, you’re not expected to start paying until your grace period ends six months after you graduate. Unlike a subsidized loan, you’ll probably graduate with a higher loan balance because your interest has been building while you’ve been in school.

If you take out an unsubsidized loan, set yourself up for success by paying off as much as you can – before the grace period even begins, if possible. By getting ahead of your interest, you’ll owe less in the long run.

See if you’re eligible for unsubsidized loans by visiting studentaid.gov.

Private Student Loans

Offered by: Private organizations like banks, credit unions, and online lenders

Pros: These loans are great for people who don’t qualify for federal loans (subsidized and unsubsidized) or if you need more money than what the government has offered you.

Cons: These tend to be more expensive than federal loans overall, though it depends on your circumstances and repayment options. You may be expected to make payments while you’re still in college, as many private loans don’t offer grace periods.

Private student loans operate more like a regular loan than a federal student loan. Like home, auto, and other loans, private loans come in all shapes and sizes:

- Some require established credit (or a cosigner), while others don’t.

- Some have fixed rates (meaning unchanging monthly payments), while others have variable rates (monthly payments can increase or decrease throughout your loan).

- Some may offer lower interest rates than federal loans, particularly if you have good credit, while others may offer significantly higher interest rates.

When to Choose a Private Student Loan

Because federal student loans generally provide more repayment help than private loans, they tend to be students’ first choice when deciding between loan types. If you’ve already looked at your federal loan options, however, and they don’t fit your needs, a private student loan could be a great choice.

You might benefit from a private student loan if:

- You didn’t receive enough federal aid to cover your tuition costs.

- You have good credit and can qualify for a lower interest rate than what’s offered federally.

- You don’t qualify for subsidized or unsubsidized loans.

- You need to pay for cost-of-living expenses that aren’t covered by federal loans, like books, groceries, and housing.

Interested in seeing your private student loan options? Browse through our student loan page to learn more about student loan basics and see which private student loans you pre-qualify for.

Find the Right Student Loan for You

Keep in mind a few things when deciding how much student loans you need to get through your degree. While it may seem easy to take out more money than is needed when declaring your loan amount, be disciplined and only take the amount you need. You’ll be glad you did when you’re done with school.

Remember to find other ways you can get financing. For example, apply for scholarships and grants or find a part-time job to help pay for school.

By figuring out what financing you will need, you can enjoy college life knowing you’re prepared for any costs that come your way.